We have been going through a tough time in this country, with the rising cost of gas, groceries, and so much more due to inflation. Keeping up with these increasing prices can feel incredibly frustrating, but there might be at least one light at the end of the tunnel that will help. Health insurance companies will be sending out rebate checks to millions of Americans. Find out why, and how much you can expect to see from your health insurance company.

The medical loss ratio provision requires insurance companies that cover individuals and small businesses to spend at least 80% of their premium income on healthcare claims and quality improvement. That means only 20% can be spent on administration and marketing expenses, or kept for profit. When private insurance companies don’t meet this standard, they are required to issue refunds to policyholders.

The rebates are calculated based on a three-year average, meaning this year’s rebates will be calculated based on the figures from the years 2019, 2020, and 2021. This year, insurance companies will be distributing an aggregate total of $1 billion to customers, down from the $2 billion issued in 2021, and a record $2.5 billion in 2020.

“In the last couple of years we’ve seen some really large rebates — twice the size of this year’s amount,” said Cynthia Cox, a vice president at the Kaiser Family Foundation and director of its Affordable Care Act program. “But I’d say $1 billion is still significant.”

How Much Can You Expect To See?

Of the $1 billion in rebates going out, the majority (an estimated $603 million), will generally go to people with a health plan through the public exchange. The refunds are expected to average $141 per participant in plans through the marketplace, $155 for those in plans through small employers, and $78 for enrollees in large-group plans. However, the rebate amount can vary widely, depending on your location and insurer.

If you’re wondering when you will see your check, get ready, because over eight million Americans can expect a rebate in the coming weeks.

As of June 17, the Affordable Care Act (ACA), also known as Obamacare, is still intact, and the long, drawn-out fights over the legislation seem to be at an end. The ACA survived its third major Supreme Court challenge with a 7-2 decision in its favor, meaning the comprehensive health care reform law will continue to provide health insurance to millions of Americans. Republican lawmakers have decided to no longer focus on repealing the law, despite election promises to end Obamacare.

In 2018, the Texas State Attorney General filed a lawsuit to have Obamacare repealed.

After former President Trump’s administration successfully challenged the individual mandate in 2017, which had meant that Americans were required to have health insurance or face a tax penalty, Texas State Attorney General Ken Paxton, a Republican, filed a lawsuit claiming that Obamacare itself was unconstitutional. His argument was that, without the tax penalty, the coverage requirement is unconstitutional, thus making the whole law unconstitutional. This battle has been going on since 2018, and the Supreme Court has finally had the chance to review the case.

Why The Lawsuit Was Dismissed

The case was decided on a technicality, with 7 justices agreeing that the challengers of the 2010 law did not have the legal right to bring the case, because the plaintiffs did not experience any harm that would give them standing to challenge the law. They did not weigh in on the constitutionality of the law.

The majority opinion stated, “Plaintiffs do not have standing to challenge [the law’s] minimum essential coverage provision because they have not shown a past or future injury fairly traceable to defendants’ conduct enforcing the specific statutory provision they attack as unconstitutional… To have standing, a plaintiff must ‘allege personal injury fairly traceable to the defendant’s allegedly unlawful conduct and likely to be redressed by the requested relief’… No plaintiff has shown such an injury ‘fairly traceable’ to the ‘allegedly unlawful conduct’ challenged here.”

Getting rid of Obamacare would have resulted in millions of Americans losing health insurance, and would have left many without the opportunity to get any; there are currently three dozen states who have opted not to establish a state exchange, so all of their residents’ only option has been to purchase an Obamacare plan. Getting rid of the law would have denied affordable health care plans to Americans whose states have refused to participate in offering exchanges.

“Congress passed the Affordable Care Act to improve health insurance markets, not to destroy them,” Chief Justice John Roberts wrote in the majority opinion.

The Future Of Obamacare

More than 25 million Americans have health insurance coverage through the ACA, and recent polling suggests that more Americans support Obamacare than oppose it. This ruling was a major win for Obamacare, and opens the door for Democratic lawmakers to extend the newly expanded subsidies for the foreseeable future, instead of allowing them to expire at the end of 2022.

“It’s our chance now to really build [on Obamacare], now that [opponents of the law have had] three strikes and…are out,” said Xavier Becerra, the secretary of Health and Human Services, and the former Attorney General of California, who stepped in with other Democratic-led states to defend the law when the Trump administration would not. “Now we know we survive, and now we build.”

Some Democratic lawmakers have taken this win as a way to push forward with universal health care coverage, but Medicare for All still faces a lot of opposition, and President Biden himself campaigned on building up Obamacare rather than pursuing a universal health care model. For now, the main focus of lawmakers is trying to make sure that Obamacare serves all Americans well.

“We’re at a moment when insurers are no longer running away from the exchanges and there’s relative stability in the individual market — and this is a moment that insurance regulators and policymakers should be asking how do your marketplace plans work better for consumers?” said Kevin Lucia, a former Obama administration health official who worked on the law’s implementation.Former President Obama agrees, saying in a tweet, “Now we need to build on the Affordable Care Act and continue to strengthen and expand it. That’s what @POTUS Biden has done through the American Rescue Plan, giving more families the peace of mind they deserve.”

Medical costs in the U.S. are high, which is why a lot of employees look for a job that offers health insurance. Over 88% of people consider health insurance benefits when choosing a job. For companies, providing group insurance to

There is no specific law that requires employers to provide health insurance coverage to their employees, but there is a penalty.

employees costs a lot of money, so some companies opt out of providing insurance. But are they required to? Yes, and no.

Affordable Healthcare Act

There is no specific law that requires employers to provide health insurance coverage to their employees. However, in January of 2015, the Affordable Care Act, ACA, required that employers who have 50 or more full-time employees provide health insurance. If they do not, they will face a tax penalty.

According to the ACA, full-time employees are employees who work an average of 50 hours a week.

Group Insurance Penalties

If a larger company with 50 or more full-time employees does not offer health insurance, they are subject to IRS penalties.

The IRS will penalize the company if one or more of their full-time employees gets a premium tax credit for getting their own health insurance coverage from the Marketplace. The company can owe up to $2,500 for each employee.

The company must offer insurance to 95% of their employees to avoid a penalty, and it must be year round. If the business offers healthcare for some months, and not others, then they will face a portion of the annual penalty.

Small Businesses

Small businesses (less than 50 employees) do not have a penalty if they do not offer health insurance to their employees.

Small businesses are not required to offer healthcare coverage to their employees. Since they have less than 50 full-time employees, they will not face penalties. If a small business does not offer health insurance, then a person can seek their own health insurance plan from the Marketplace or a private company.

While there is no longer a penalty for going without healthcare coverage, it is important to seek out information on different plans. There are plans within your budget that will meet your needs and lifestyle. If you need help searching and comparing all the group insurance plans around, EZ.Insure can help. We offer local specialized insurance agents that can do all the comparisons for you, and just provide you the quotes. All for free! It’s that simple. To begin, enter your zip code in the bar above, or to speak to an agent, email replies@ez.insure, or call 888-998-2027. There is no hassle involved, and no obligation to buy, and no headaches. Just easy, fast, and free quotes!

The Affordable Care Act is once again facing a new challenge, this time by Republican states trying to dismantle it once and for all. The basis of the claim filed is that since the individual mandate was removed, it makes the whole ACA unconstitutional. The individual mandate is the ruling that people must have insurance or sign up for it within an amount of time or they would face a penalty fine during tax season.

Ever since President Trump was elected, one of his goals was to repeal and replace the Affordable Care Act which was signed into law by President Obama in 2010. One of the provisions of the ACA, the individual mandate, has been challenged by Republicans since 2012. They claimed it was an unconstitutional expansion of the government’s power. However, the Supreme Court upheld that the individual mandate tax was the government’s right. Chief Justice John G. Roberts Jr. stated the government “does not have the power to order people to buy health insurance, but it does have the power to impose a tax on those without health insurance.”

In December 2017, President Trump came one step closer to dismantling the ACA by ridding the mandate. His administration was able to change the individual mandate penalty to $0 beginning January 1, 2019. Because of this, as of February 26, 2018, Texas Attorney General Ken Paxton and 19 other states filed a lawsuit stating, “the country is left with an individual mandate to buy health insurance that lacks any constitutional basis. . . . Once the heart of the ACA — the individual mandate — is declared unconstitutional, the remainder of the ACA must also fall.”

In one of the cases against the ACA, King v. Burwell, Chief Justice John G. Roberts Jr. noted that “Congress passed the Affordable Care Act to improve health insurance markets, not to destroy them. If at all possible we must interpret the Act in a way that is consistent with the former and avoids the latter.”

Judge Reed O’Connor will be hearing the case filed by the Texas Attorney General and other states. O’Connor was appointed by President George W. Bush in 2007 and has ruled against the ACA in past cases.

This is all happening during the time insurers must figure out the pricing for next year’s premiums and rates so they can file it with state regulators. Insurers are concerned because they do not know how much to raise rates if they will charge the same price to healthy and sick people, or whether to pull out of the marketplace.

While the marketplace in in panic about how much their prices should go up and if they will even still be in business, it is smart to seek quotes and plans from private insurers. EZ.Insure is able to provide you with affordable plans with ease. We offer the stability of insurance within your region by one of our highly trained and educated agents. To receive a quote, call 855-220-1144 to speak your own advisor, enter your zip code in the bar above, or email us at replies@ez.insure. We will provide quotes and offer our help free of charge without hassle.

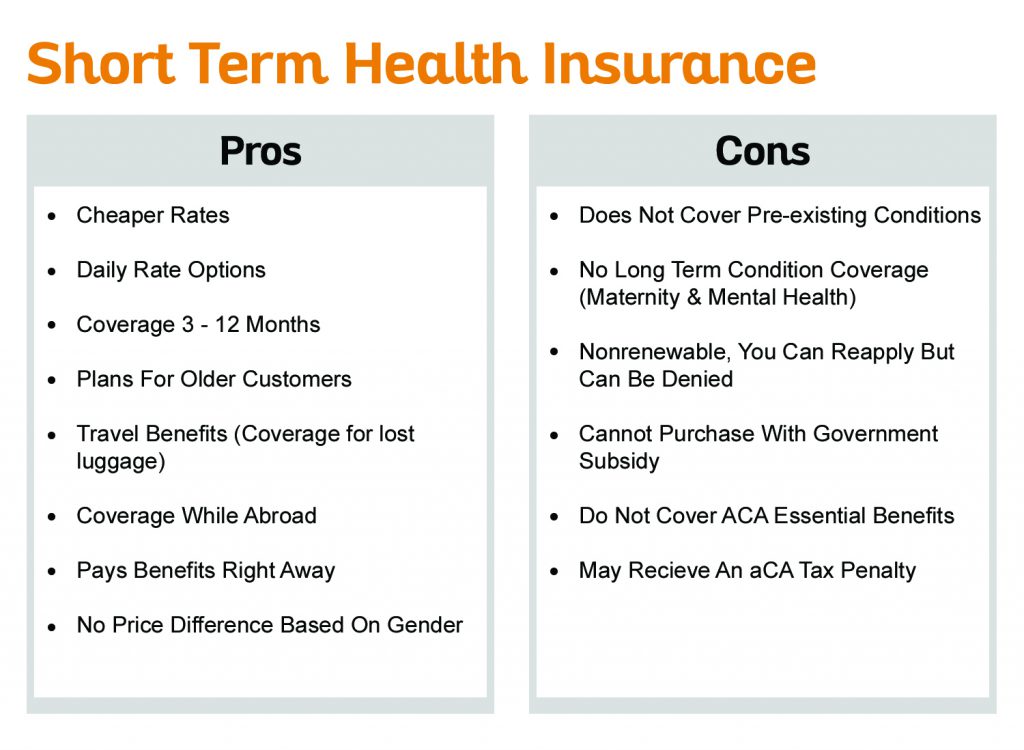

When it comes to determining if a short-term health insurance plan or a major medical health insurance is best for you, there are many factors you must consider. Two of the main things to consider are how long you want coverage and what you want to be covered. Short-term plans aid people when a catastrophic issue arises, such as a sudden injury or illness. With short-term health insurance, you can choose how long you need coverage, and what price you want to pay. Major medical health insurance provides more comprehensive care than short term insurance. Major medical plans include things such as preventative care and wellness checks. Unlike short term plans major medical plans lasts longer than a year and are usually more expensive.

Short-Term Health Insurance

The purpose of a short-term plan is to cover medical and travel expenses from 3 – 12 months. These health insurance plans are also called travel insurance plans because if you are traveling outside of the US, short-term plans will offer you basic coverage for a limited time.

Short-term plans are a more flexible option for people looking for coverage for no longer than a year. Short-term plans, unlike regular health insurance plans, are charged a daily rate which lets you buy a plan for the time you need, whether it be a month or more. The plan can go into affect anywhere from the day after applying to 14 days later. These insurance plans are generally nonrenewable, but you can reapply if needed with some restrictions.

Short-term plans are usually up to 50% cheaper than long-term plans. Savings vary by person, for example, a man who does not smoke can purchase the cheapest short-term plan for $110 a month, while the cheapest long-term plan will cost him about $270 a month. The savings are even more significant if you are under the age of 30 and plan on traveling out of the United States. People under the age of 30 can get short term health insurance plans for as low as $38 a month.

These plans are less expensive and much easier to obtain. The application does not require a medical exam and only asks a handful of yes or no health questions in order to get approved. Short term health insurance plans, unlike normal health insurance plans, also offer plans for older customers. You can apply for a plan up to the age of 89, while normal health insurance plans are not offered after age 75.

Pros & Cons of short term health insurance

Who Should Apply For Short Term Health Plans

According to the National Association of Insurance Commissioners, short-term policy utilization has increased from 108,000 people in 2013 to 148,000 people in 2015. Short-term plans have been gaining popularity among those who need coverage but cannot afford long-term health insurance. It is ideal for anyone who waited too long to purchase long-term and missed the open enrollment period, young adults who can no longer be on their parents’ health plans, people in between jobs, and those that are waiting for their employer or government benefits to begin. Some people buy short-term insurance to cover the deductible period before their long-term insurance starts paying. Others purchase these plans to fill in the gaps of Medicare coverage.

Major Medical Health Insurance

Major medical insurance is a long-term plan that offers more comprehensive coverage. These plans help manage day to day expenses and are convenient for those that require routine medical work , such as medication, lab work, and inpatient and outpatient services. Major medical health insurance complies with the ACA requirements which means it provides the ten essential health benefits. These ten essential benefits are: ambulatory patient services, prescription drugs, emergency care, mental health services, hospitalization, rehabilitative services, preventative and wellness services, laboratory services, pediatric care, and maternity and newborn care. However, most health insurance plans do not cover dental, vision and hearing, so you must purchase a separate plan for any of these forms of coverage.

Major medical policies offer peace of mind in knowing that you are covered in case of emergency or future conditions. These plans allow you to choose your own policy and deductible, but require you to answer health questions and conduct a medical exam to determine if you are qualified for benefits. Your policy rates depend on your age, gender, marital status, and the amount of coverage you desire. As of January 1, 2014, people who purchase major medical plans cannot be turned down or have rates raised due to pre-existing conditions.

Unlike short-term health insurance plans, major medical plans offer more extensive coverage and you will not be issued a tax penalty because it abides by ACA guidelines. These plans can be renewed annually unlike short-term plans which only last up to a year. You must enroll during open enrollment which is from November 1st to December 15 this year. If you miss open enrollment, then you will have to wait until the next enrollment period, unless you qualify for special enrollment. These special circumstances are when you adopt or have a child, get married, lose coverage from an employer, or move outside network area. If you attempt to purchase a plan outside of open enrollment, it will cost you a lot more.

Major Medical Health Insurance Pros & Cons

Who Should Apply For A Major Medical Health Plan

Major medical insurance is important to have for everyday health coverage, for both an individual or a family. It helps people whose employer or spouse’s employer does not offer health insurance. If you are pregnant or planning to become pregnant, this plan is your best option because it will cover your medical expenses and the newborn is generally put on the plan automatically. Short term health plans do not offer any type of coverage for pregnancy expenses. When you are over 26 years old and are no longer on your parent’s plan, then a major medical plan is best if you are looking for preventative care and wellness checks.

If you need help comparing different types of health insurance plans EZ.Insure will help you. We will connect you with a highly trained agent that will help you discover what health insurance plan is best for you. To get started, you can put your zip code in the link to the right, email us at replies@ez.insure, or give us a call at 855-400-0489.

Shortened Open Enrollment Period- When Is The Deadline & What This Means For You

This year the government has decided to shorten the Open Enrollment Period from three months to only six weeks, lasting from November 1, 2017 to December 15, 2017. If you sign up during this period, coverage does not start immediately, it begins January 1, 2018. With a shortened amount of time, it is important to be diligent and look into plans as early as possible. If not, you can end up getting stuck with a plan that does not suit your needs, or even worse, miss out on signing up for a plan altogether.

Some states have extended their open enrollment period to allow people more time in choosing a plan. These nine states are highlighted on the map below:

2017 Open Enrollment Period has been shortened in most states. Only 9 States have extended deadlines.

California – November 1, 2017 to Jan. 31, 2018

Colorado – November 1, 2017 to Jan. 12, 2018

Connecticut – November 1, 2017 to December 22, 2017

District of Columbia – November 1, 2017 to Jan. 31, 2018

Florida – November 1, 2017 to Dec. 31, 2017

Massachusetts – November 1, 2017 to January 31, 2018

Minnesota – November 1, 2017 to January 14, 2018

New York – November 1, 2017 to January 31, 2018

Rhode Island – November 1, 2017 to December 31, 2017

Washington – November 1, 2017 to January 15, 2018

Select Georgia Counties – November 1, 2017 to Dec. 31, 2017

Not all states can change their open enrollment period, but there are three more states that can extend at anytime. These three states are Idaho, Maryland, and Vermont.

Not only has the open enrollment time been reduced, but there are also added provisions

1. Special Enrollment Period- When the open enrollment period is over, people may enroll during the special enrollment period. These circumstances are such as when you adopt or have a child, get married, lose coverage from employer, or move outside network area. With the change of a shorter enrollment period, came a stricter ruling on special enrollment. Now you need to send documentation in a short period of time to prove your circumstance, whereas before they just took your word on it. 2. Non Payment Loopholes Removed- Some people learned a loophole to save money during open enrollment. They would stop paying their premium in the months leading up to enrollment so their plan gets cancelled. But now with new provisions, you cannot switch coverage unless your old coverage is paid in full. Due to this rule, a lot of people who are behind on payments will not be able to sign up.

How Does This Affect You

In the previous year, when the open enrollment period was 3 months, more people signed up later in the open enrollment period. During the second half of the 3 months (about 7-12 weeks) is when 60% of new enrollments occurred and when people switched plans. With only 6 weeks open, people are forced to make a quicker decision in choosing a plan, and some might miss out completely. Enrollees who signed up in January, and had a Feb. 1 effective date, were healthier on average than those with a Jan. 1 effective date. People who are healthy may procrastinate and miss out on open enrollment this period, and these healthy procrastinators are the ones who balance the risk pool and lower premiums.

How This Will Affect The Healthcare System

Insurers do not favor longer open enrollment periods. This is because people will wait until they are sick before they apply for coverage, and then insurers will have to cover their pre-existing conditions. Insurance companies fear of going broke due to all the sick individuals they must cover. If the healthy procrastinators do not sign up because they missed the opportunity, then the premiums will go up in order to cover those who are sick.

Given the shorter amount of time to sign up for insurance, it is very important to go over plans and choose the best one for you, rather than making a rushed decision. In order to better prepare yourself, you need to consider some things when purchasing a health insurance plan. You need to consider past health needs, future health needs, pharmaceutical needs, and your financial situation. Ez.Insure will help you choose the plan that suits all those needs. Simply put your zip code in the bar above to get started, or contact us through email at Replies@ez.insure or call 888-350-1890 . One of our agents are always ready to help you at no charge, with no obligation.

In December 2017, President Trump came one step closer to dismantling the ACA by ridding the mandate. His administration was able to change the individual mandate penalty to $0 beginning January 1, 2019. Because of this, as of February 26, 2018, Texas Attorney General Ken Paxton and 19 other states filed a lawsuit stating

In December 2017, President Trump came one step closer to dismantling the ACA by ridding the mandate. His administration was able to change the individual mandate penalty to $0 beginning January 1, 2019. Because of this, as of February 26, 2018, Texas Attorney General Ken Paxton and 19 other states filed a lawsuit stating