Inflation has been on the rise for some time now, and it doesn’t look like it’s going to be slowing down anytime soon. The rising costs of gas and groceries have been tough on many Americans, and as if that wasn’t enough, health insurance premiums are now expected to increase, as well. The reasons for the increase include the effects of the pandemic, shrinking tax credits, prices set by drug manufacturers, and other health care costs. And unless Congress extends the expanded subsidies for Marketplace coverage, premiums could increase by 50% for some. Don’t panic yet, though: there are ways that you can save.

Tax Credits Disappearing

The American Rescue Plan Act, which was signed into law in March 2021, allowed Americans earning any amount of money to enjoy tax credits or premium subsidies, and also capped the amount that anyone pays for premiums at 8.5% of their income. Unfortunately, though, Congress put a two-year limit on these provisions, and at the end of this time, premiums are set to rise by more than 50% on average for people getting health coverage through a Marketplace plan.

“The default is that the expanded subsidies will expire at the end of this year,” said Cynthia Cox, a vice president at the Kaiser Family Foundation and director of its Affordable Care Act program. “On average, premiums would go up more than 50%, but for some, it will be more.”

And if Congress does not extend the expanded tax credits, only people with household incomes of 100% to 400% of the federal poverty level will qualify for subsidies.

Increases in Drug Prices

What’s making the problem worse is that the prices of new drugs in the U.S. have climbed for more than a decade. According to a research letter published in the Journal of the American Medical Association, the launch prices of new brand-name drugs increased by nearly 11% every year from 2008 through 2021.

Eric Linzer, President and CEO of the NY Health Plan Association, says state legislatures are also contributing to higher premium costs, specifically with bills that prohibit any kind of change in health plan formularies (or the list of prescription drugs covered by insurance plans). For example, Bill S.4111/A.4668 would prohibit health insurance plans from making mid-year pharmacy formulary changes, resulting in higher health insurance premiums and exacerbating the increasing cost of drugs.

In addition, several states have passed legislation that prohibits the use of copay accumulator adjustment programs (CAAP), or accumulator adjustment programs. These programs seek to reverse the impact of manufacturer cost-sharing assistance for prescription drugs by not counting the manufacturer assistance amount towards a patient’s deductible and out-of-pocket maximums. If the co-pay assistance is not counted against the patient’s deductibles and coinsurance amounts, it will drive up the patient’s health care costs overall.

“If we’re going to get those costs under control and make premiums more affordable for individuals and employers it’s important that policymakers look at what the underlying costs are. 82% or more of the premium dollar goes to pay for doctors visits, hospital stays, prescription drug costs,” said Linzer.

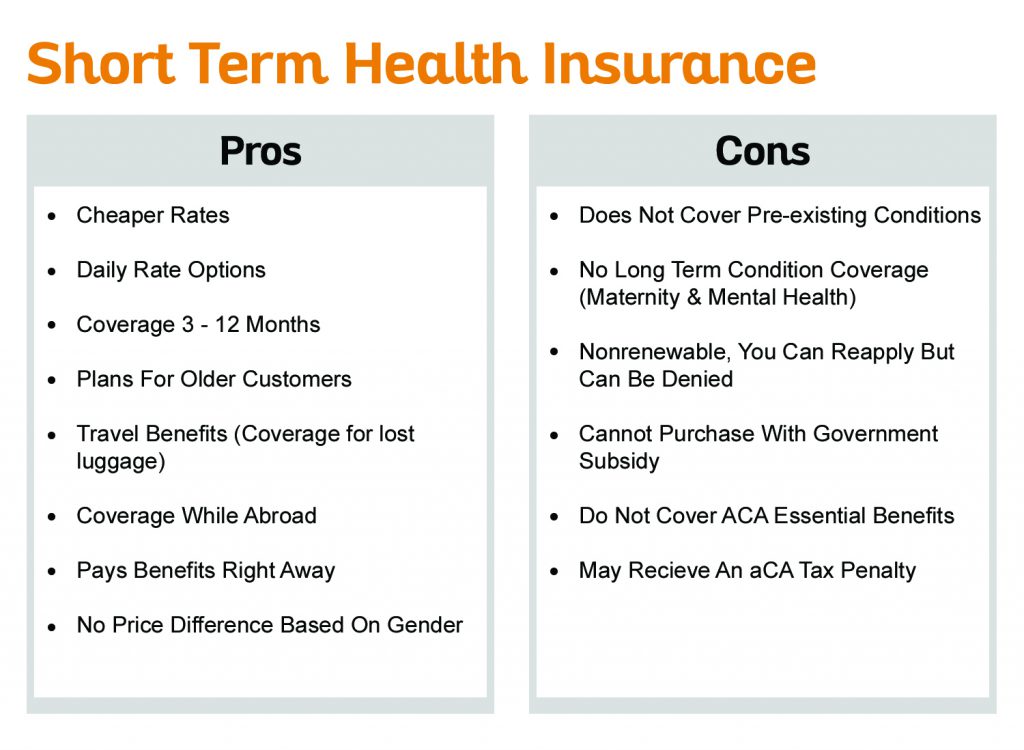

Find Affordable Health Insurance

Even though health insurance costs are rising, it doesn’t mean you can’t find an affordable plan that provides the coverage you need. And remember, it’s always better to get a plan before an accident happens, or a chronic condition develops or worsens.

EZ provides you with easy, instant, accurate quotes with no strings attached. Your own personal advisor will provide you with instant quotes and a comparison of all the other top plans available. Not only will you save time and money, but you also won’t have to pay us a cent for our services. We have the technology and network to cut hours of time spent comparing plans down to seconds. When you visit our site, you’ll leave with complete details and comparisons from dozens of plans available to you. These come from our team of experts, who filter all insurance plans to find the most suitable to your health needs and budget.

Don’t waste any more time missing out on savings! To get your instant quotes, enter your zip code in the bar above, or to speak to an agent, call 888-350-1890.